When Franco left as Spain's Ruler, Spain was in good shape economically. But, the people of Spain listened to the siren song of Social Democracy and the temptation of getting something for nothing set them on a path to ruin. It did not happen overnite. Candidates for election vied with each other to deliver more. With each delivery of something for nothing (or for something run by the government), the overall health of the country grew less robust, untill the election of a Socialist government. Spain's Socialists fought the phantom war on global warming, creating expencive energy, less competitive industry and greater national debt to continue government spending.

The Socialists were defeated in the last election and Spain tried to revert to what was happening before the Socialist government. But, Social Democracy (Soft Socialism) is also a path to failure. Spain's debts grew to unsustainable levels.

That's when the ECB intervened. In fact, the ECB forced Spain to reduce government spending and raise taxes - not a lot, but still the reduction in spending and the increase in taxes were supposed to mreduce the deficit. It didn't happen. Why? Because the reduced spending and increased taxes created a fiscal cliff and Spain's recession deepened. That, of course, increased the deficits.

So, what is the lesson for us? Will we have a fiscal cliff? Hard to tell. If Obama is re-elected, we certainly will, because Obama wants higher taxes on higher earners. Please remember that contrary to the demagoguery, wealth is not taxed. IT IS CALLED AN income tax BECAUSE IT IS INCOME THAT'S TAXED. If Romney wins, his instinct is to cooperate with the Dems and the Dems want higher taxes. Will a Republican House agree? Unknown.

Central to the Romney plan is to increase oil and gas production and to tame the EPA. Having cheap energy and plenty of it will eliminate China's adventage of cheap labor, but this effect will take years. In the meantime, the Democrats can demagogue, sabotage and slow the economic recovery if they can. A fiscal cliff and a recession would certainly fuel Pelosi's hopes of growing the economy with unemployment checks.

Tuesday, October 30, 2012

Monday, October 29, 2012

Attention now switches to France.

We have seen the PIIGS (Portugal, Italy, Ireland, Greece and Spain) come to the agonizing realization that the Day of Reckoning has arrived. Soft Socialism has run out of other people's money to redistribute and these governments have run their credit dry. Weak economic growth has dipped into deep recessions with unemployment hovering at 25%. Huge public debts and struggling businesses are not accidents but the consequence of Social Democracy; what I call Soft Socialism. It is fitting that among the young, who have been miseducated to be big supporters of Socialism, unemployment is even higher, 50%.

It then comes as no surprise that one of the architects of Soft Socialism (France) is now coming to attention as it faces its own Day of Reckoning. The French people did the (to them) logical thing: put the Socialists in charge of reforming Socialism. And what has Mr Francois Hollande, France's Socialist President decided to do to make France more competitive? He and his Party did what you can expect Socialists to do: 1. had lots of meetings, 2. added more government in the form of a new Ministry (the Ministry of Industrial Recovery), 3. raised taxes on high earners and 4. and asked a sympathetic businessman (Luis Gallois, former Chairman of Airbus) to draw up plans to make France more competitive. So, how does the French version of hope and change coming? Well, the plans drawn up by Monsieur Gallois have been filed in the place where all such plans are filed, several high profile high earners have left France for friendlier countries (expect tax receipts to fall) and big businesses have concluded that there is no point to hire more workers.

What about the obstacles to productivity, which are: Rigid work rules, including the 35-hour week, high administrative costs, strict government oversight of layoffs and generous severance when job loss is inevitable. The upshot is an effective tax rate of more than 60 percent on corporate profits, once all the expenses are tallied. How about the reforms suggested by Mr Gallois: increase the work week, shift some of the tax burden to the workers and reduce government spending? President Hollande is quoted as "I'd advise against the idea of a shock, which has more of an attention-getting effect than a real therapeutic effect," Hollande said Thursday. Without offering details, he said he would prefer a "pact" among the government, workers and employers.

Pres Hollande is like the Father in the European fairytale, who was offered money for one of his children, but he could not part with any, because he loved them all. The obstacles to productivity are the children of the Left and they are all precious to the Left, because they define who the Left are. The obstacles to productivity took decades to put in place and will not be removed if the Left has a way to preserve them.

But, time is running out. Standard and Poor downgraded the biggest French bank BNP Paribas last Thursday and the stage is set to usher in more unpleasant surprises.

It then comes as no surprise that one of the architects of Soft Socialism (France) is now coming to attention as it faces its own Day of Reckoning. The French people did the (to them) logical thing: put the Socialists in charge of reforming Socialism. And what has Mr Francois Hollande, France's Socialist President decided to do to make France more competitive? He and his Party did what you can expect Socialists to do: 1. had lots of meetings, 2. added more government in the form of a new Ministry (the Ministry of Industrial Recovery), 3. raised taxes on high earners and 4. and asked a sympathetic businessman (Luis Gallois, former Chairman of Airbus) to draw up plans to make France more competitive. So, how does the French version of hope and change coming? Well, the plans drawn up by Monsieur Gallois have been filed in the place where all such plans are filed, several high profile high earners have left France for friendlier countries (expect tax receipts to fall) and big businesses have concluded that there is no point to hire more workers.

What about the obstacles to productivity, which are: Rigid work rules, including the 35-hour week, high administrative costs, strict government oversight of layoffs and generous severance when job loss is inevitable. The upshot is an effective tax rate of more than 60 percent on corporate profits, once all the expenses are tallied. How about the reforms suggested by Mr Gallois: increase the work week, shift some of the tax burden to the workers and reduce government spending? President Hollande is quoted as "I'd advise against the idea of a shock, which has more of an attention-getting effect than a real therapeutic effect," Hollande said Thursday. Without offering details, he said he would prefer a "pact" among the government, workers and employers.

Pres Hollande is like the Father in the European fairytale, who was offered money for one of his children, but he could not part with any, because he loved them all. The obstacles to productivity are the children of the Left and they are all precious to the Left, because they define who the Left are. The obstacles to productivity took decades to put in place and will not be removed if the Left has a way to preserve them.

But, time is running out. Standard and Poor downgraded the biggest French bank BNP Paribas last Thursday and the stage is set to usher in more unpleasant surprises.

Thursday, October 25, 2012

German gold hoard is gone

says James Turk in an article today on KWN:

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2012/10/25_James_Turk_-_The_Entire_German_Gold_Hoard_Is_Gone.html

Turk discusses the role of ESF (Exchange Stabilization Fund and its involvment in the gold market. He also rips away part of the financial curtain of how gold price is manipulated.

http://kingworldnews.com/kingworldnews/KWN_DailyWeb/Entries/2012/10/25_James_Turk_-_The_Entire_German_Gold_Hoard_Is_Gone.html

Turk discusses the role of ESF (Exchange Stabilization Fund and its involvment in the gold market. He also rips away part of the financial curtain of how gold price is manipulated.

Wednesday, October 24, 2012

Bernanke's crimes.

FED Chairman Bernanke is rumored to be leaving. Mitt Romney has already said he did not want Bernanke reappointed.

The title of this post accuses Bernanke of crimes. Am I justified in referring to Bernanke's actions as crimes, as opposed to being real stupid? I believe so. And here is why: 1. Bernanke's FED imposed 'mark to market rules' in Sep 2008. This made the banks insolvent, elected Obama and started the bailout orgy; 2. Bernanke's FED has been creating insane amounts of money that threatens the end of the US Dollar; 3. The purpose of the FED creating money is to stimulate the banks to increase lending, thus spur on the economy; 4. While the FED has increased the amount of money given to the banks, Bernanke is sabotaging bank lending by having increased reserve requirements and paying the banks for not lending. The money then ends up lifting the stocks even while earnings are decreasing. As soon as the banks are no longer given the risk-free money, it will flood the market creating inflation.

I have posted similar comments before. Why post it again? Because I have a post from Weiss Research that says practically the same thing. Here are exrpts:

"

This means that, instead of creating liquidity and spurring lending, the banks are putting the cash in a big vault for a rainy day.

Just consider that, in the last five years, consumer revolving credit — money being loaned by banks for things like credit cards — has fallen 16% while the Fed has flooded the markets with more than $1.6 trillion in QE money.

Because consumers can’t get credit, the standard supply-and-demand curve is kicking in. After all, we need cash right now to buy businesses ... cars ... and plenty more.

Investors don’t realize this yet. The majority think the Fed’s printing is being injected directly into the economy.

Instead, the financial institutions are fattening their balance sheets ...

Since 2008, the Fed has been paying banks a fixed interest rate of 0.25% for excess reserves.

While this doesn’t sound like much at a glance, consider that the Federal Funds rate has recently dipped as low as 0.13% and that GDP growth is projected to be as low as 1.75% for 2013.

All of this makes a risk-free 0.25% appealing indeed.

To top it off, the Fed is keeping a tight reserve requirement — which, coupled with the interest on excess reserves — creates incentive for banks not to lend."

Why?

Why?

Because that money is helping the financial institutions buoy the markets.

For example ... in a recent study, Standard & Poor’s showed a quarterly decline in gross earnings of 2.6%. However, when financials were removed ... this number almost doubled to 5%.

And it’s not just here in the United States.

After seven years of increased lending, the euro zone’s consumer credit is beginning a slow decline. Since 2010, credit lending has fallen 6%.

This stagnancy in credit is causing people to double-down on their dollars ... and as a result, we’re seeing an overall slowdown in transactions.

The U.S. Velocity of Money indicator — which measures the speed of transactions to buy and sell products — has fallen 16% since 2007. In Europe, it has fallen 14% since 2007.

All of this is temporarily driving up fiat currencies."

So, Bernanke risks our financial system by printing money, while deliberately sabotaging the effect of the printed money on the economy.

The title of this post accuses Bernanke of crimes. Am I justified in referring to Bernanke's actions as crimes, as opposed to being real stupid? I believe so. And here is why: 1. Bernanke's FED imposed 'mark to market rules' in Sep 2008. This made the banks insolvent, elected Obama and started the bailout orgy; 2. Bernanke's FED has been creating insane amounts of money that threatens the end of the US Dollar; 3. The purpose of the FED creating money is to stimulate the banks to increase lending, thus spur on the economy; 4. While the FED has increased the amount of money given to the banks, Bernanke is sabotaging bank lending by having increased reserve requirements and paying the banks for not lending. The money then ends up lifting the stocks even while earnings are decreasing. As soon as the banks are no longer given the risk-free money, it will flood the market creating inflation.

I have posted similar comments before. Why post it again? Because I have a post from Weiss Research that says practically the same thing. Here are exrpts:

"

The Fed Is Telling Banks to Hoard Their Cash!

This means that, instead of creating liquidity and spurring lending, the banks are putting the cash in a big vault for a rainy day.

Just consider that, in the last five years, consumer revolving credit — money being loaned by banks for things like credit cards — has fallen 16% while the Fed has flooded the markets with more than $1.6 trillion in QE money.

Because consumers can’t get credit, the standard supply-and-demand curve is kicking in. After all, we need cash right now to buy businesses ... cars ... and plenty more.

Investors don’t realize this yet. The majority think the Fed’s printing is being injected directly into the economy.

Instead, the financial institutions are fattening their balance sheets ...

And the Fed is exacerbating this problem by paying banks not to lend!

Since 2008, the Fed has been paying banks a fixed interest rate of 0.25% for excess reserves.

While this doesn’t sound like much at a glance, consider that the Federal Funds rate has recently dipped as low as 0.13% and that GDP growth is projected to be as low as 1.75% for 2013.

All of this makes a risk-free 0.25% appealing indeed.

To top it off, the Fed is keeping a tight reserve requirement — which, coupled with the interest on excess reserves — creates incentive for banks not to lend."

Why?

Why?

Because that money is helping the financial institutions buoy the markets.

For example ... in a recent study, Standard & Poor’s showed a quarterly decline in gross earnings of 2.6%. However, when financials were removed ... this number almost doubled to 5%.

And it’s not just here in the United States.

After seven years of increased lending, the euro zone’s consumer credit is beginning a slow decline. Since 2010, credit lending has fallen 6%.

This stagnancy in credit is causing people to double-down on their dollars ... and as a result, we’re seeing an overall slowdown in transactions.

The U.S. Velocity of Money indicator — which measures the speed of transactions to buy and sell products — has fallen 16% since 2007. In Europe, it has fallen 14% since 2007.

All of this is temporarily driving up fiat currencies."

So, Bernanke risks our financial system by printing money, while deliberately sabotaging the effect of the printed money on the economy.

Monday, October 22, 2012

Islamic Banking.

The latest post from Larry offers this as an out of the debt-burdened economy of the West: 1. monetize all debt and 2. institute a banking system that resembles Islamic Banking. What is Islamic Banking? Here is a description of how it conducts banking and what it is aimed at:

be too late….and the US isn’t far behind, unless they wake up.

What is Sharia Banking?

By: John L. Terry, III

London is the leading Islamic banking center in the West, and the Netherlands is seeking to overtake

London in this regard. Wall Street is becoming enamored with Islamic banking (also known as Sharia

banking) and this banking model is rapidly gaining acceptance in the Western world.

Unlike the traditional banking model most Westerners are familiar with, Islamic banks are managed

according to Sharia law. The main difference between Western banking and Islamic banking is the

Quran prohibits the collection of interest in all monetary transactions, charging fees (and donations) for

services provided in lieu of charging interest on loaned capital.

Islamic banks are also governed by a Sharia Advisory Board, which is comprised of Islamic scholars and

clerics who are responsible to ensure all of the bank’s activities are in strict compliance with Sharia

(Islamic) law. Those in favor of Islamic banking believe the Islamic banking system is superior to the

capitalistic model of the West, because it is structured around a “strict code of ethics” (based on the

Quran) and is prohibited from “exploitative practices” (including the charging of interest).

According to Islamic banking proponents, this allows banking to be an integral part of a moral society

(governed by the Quran). In contrast, they believe capitalism is solely focused on money (profit) and

this incites greed and the exploitation of others, which leads to the social problems in the West,

including the division of classes and unequal distribution of wealth. They also believe the Islamic

banking model would rid the West of these social problems and bring about a more equitable and fair

society.

Many of the scholars and clerics who sit on these Islamic Banking Advisory Boards come from the more radical elements of Islam, and the educational centers that promote and encourage violence against the West. According to the

Brussels Journal, these groups have openly expressed hopes of returning Islam

to Europe “as a conqueror” either by preaching and ideological change or “by the sword”.

Islamic banks now position themselves as the moral alternative to Western banks, and 3 in 4 Muslims in England prefer sharia

‐compliant banking products over their Western banking counterparts. In Europe,

Islamic banking is now reaching beyond the Muslim community, seeking to become the preferred choice

of non

‐Muslims for banking transactions, citing their products (and banking ethics) are superior to the

Western banking system. In London alone, some 20% of inquiries into Islamic banking products is now

coming from non

‐Muslims.

As Sharia banking becomes increasingly accepted as an alternative to the Western model, the

opportunity to spread Islamic ideology to non

‐Muslims increases. According to Sheik Yousef Al‐

Quardawi (a leading Sunni cleric, spiritual leader of the Muslim Brotherhood, and head of the

fundamentalist European Council for Fatwa and Research), the introduction of Islamic banking into the

West will be the vehicle through which Islam will establish a caliphate (Islamic government rule based

on the Quran) throughout the world.

According to

Helena Christofi of The Brussels Journal, “Replacing western institutions with a global

Islamic order is, in fact, the goal of Al

‐Qaradawi’s Muslim Brotherhood. According to its founder, Hassan

The Revelation Files PO Box 640 Russellville AR 72811

www.revelationfiles.com

Al

‐Bana, the Brotherhood seeks to “[reclaim] Islam’s manifest destiny; an empire, founded in the

seventh century, that stretched from Spain to Indonesia,” and its 1982 “secret plan” exhorted its

members “to channel thought, education and action in order to establish an Islamic power on the

earth.” The Muslim Brotherhood is a central link between Islamic banking and Islamic fundamentalism;

the first Islamic bankers were members of the Muslim Brotherhood who wanted to use “the structural

power of bank ownership” to advance the fundamentalist movement in the Gulf States in the 1970s.

Today, its most powerful progeny, the Kuwait Finance House, covertly finances fundamentalist groups in

Kuwait and abroad.”

To educate the West, the Islamic Bank USA has created a website (

www.islamic‐bank‐usa.com) to

inform non

‐Muslims about Sharia banking. According to their website, Sharia compliant banking

products must be:

1. Interest free

2. Trade

‐related with a genuine need for the fund in its purest form, so it is therefore equityrelated.

3. Ethically directed. Certain areas of finance are permitted, while others are not. For example,

funds cannot be provided for liquor, pork, gambling, pornography and anything that Islamic law

deems unlawful.

Most products offered through Islamic banks include a profit (mark

‐up) rather than charging interest on

the amount at risk. Islamic banking prohibits trading in debt, so Islamic banks do not issue conventional

bonds. Islamic bonds are not interest based, but returns are based on a mathematical formula that links

the cash flow (that will be generated by the asset to be purchased) to the cost of the asset itself.

Sharia banking law also requires that a portion of all fees (by some accounts, 20% or more) collected be

paid to Islamic charities, which are often fronts for terror organizations (according to Western

intelligence sources). This has proven to be a major funding source to move profits from the West to

Islamic organizations, and effectively aids in the redistribution of wealth to the Middle East.

WorldNetDaily

recently reported concerns expressed by the US Treasury over potential ramifications of

Islamic banking institutions seeking to make substantial investments in Western (i.e. US) banks and

securities firms. As Islamic institutions gain a financial foothold in the Western banking and investment

community, they could exert political pressure or force these institutions to offer Sharia

‐compliant

banking products (which in turn further solidifies Islamic ideology into the West).

Should Sharia banking become the accepted form of commerce in the Western world, the Islamic clerics

would have a powerful platform to espouse their ideology and significantly alter how life in the West is

lived. The influence and control Sharia banking could impose on life in the US, both in the governmental

and private sectors, is considerable.

And once financial control is wrested from the Western banking system, the Golden Rule of Finance

becomes the governor of life.

The Golden Rule of Finance simply states, “He who has the gold, makes the rules.” For Europe, it may

be too late….and the US isn’t far behind, unless they wake up.

Friday, October 19, 2012

The latest European Summit.

EU leaders are meeting again. It will not be their last meeting of the year, there will be another before the end of the year. In case u r interested in the details of the meeting and how the meeting is viewed from the various capitols, the best place to go for a read is:

http://www.economist.com/blogs/charlemagne/2012/10/eu-summit-0

There have been two topics so far: 1. the EU Bank Supervisor and 2. who will represent the EU to accept the by now farcical Nobel Peace Prize. We can dismiss topic "2" as of little importance and blog about topic "1."

The EU Bank Supervisor was a German idea aimed at forcing the various EU nenbers to live within their means. The Summit accepted the idea, but the details are yet to be worked out. So, when will the EU have such a Supervisor? Starting next year. The Germans are insisting on quality, the French are urging speed.

http://www.economist.com/blogs/charlemagne/2012/10/eu-summit-0

There have been two topics so far: 1. the EU Bank Supervisor and 2. who will represent the EU to accept the by now farcical Nobel Peace Prize. We can dismiss topic "2" as of little importance and blog about topic "1."

The EU Bank Supervisor was a German idea aimed at forcing the various EU nenbers to live within their means. The Summit accepted the idea, but the details are yet to be worked out. So, when will the EU have such a Supervisor? Starting next year. The Germans are insisting on quality, the French are urging speed.

Thursday, October 18, 2012

The Invisible Crash.

This is a term that has been applied by the Oxford Club Economists to describe what is happening today.

What is this "Silent Crash?"

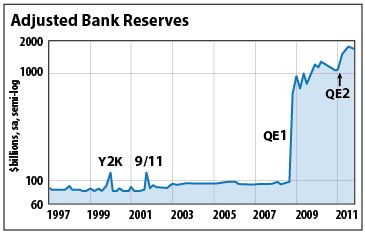

The Obama regime's Economists talk about a "recovery" as they look at the scene. A lot of people see the crash coming, but few know that it is already happening. First, let's look at the adjusted bank reserves. This graph tells us that bank reserves increased by a factor of ten! That means that monetary inflation is rampant.

The regime's supporters are quick to point out that that prices have not changed much. In fact, they point to the DOW as proof that their policies created a recovery. That is deceptive. The US Dollar has lost over 90% of its purchasing power during the last 100 years and is headed for more Trouble.

The regime's supporters are quick to point out that that prices have not changed much. In fact, they point to the DOW as proof that their policies created a recovery. That is deceptive. The US Dollar has lost over 90% of its purchasing power during the last 100 years and is headed for more Trouble.

What is this "Silent Crash?"

The Obama regime's Economists talk about a "recovery" as they look at the scene. A lot of people see the crash coming, but few know that it is already happening. First, let's look at the adjusted bank reserves. This graph tells us that bank reserves increased by a factor of ten! That means that monetary inflation is rampant.

The supporters of the Obama regime and the FED claim success

in inflating the DOW 45% from 2009 to 2012. In terms of gold, however, the DOW

is down 16%,and in terms of metals in general it is down 21%. In terms of

cotton, the DOW dropped 16%,and 14% in terms of dairy and 46% in terms of oil.

We as yet do not see a general inflation in general prices

and this is due to the "Time Lag Effect of Price Inflation."

Businesses are reluctant to pass on the increases in commodities, but the day

will come when they have no choice. Then prices will explode. And bonds and

Treasuries will lose their value almost overnight. Stocks in general will lag

inflation.

All this will be made worse if we fall off the fiscal cliff

or there is a grand bargain to raise taxes and leave Obamacare in place.

The world's second biggest Ponzi scheme.

Sorry London Trader, but the "Biggest" Ponzi scheme is reserved for the Social Security in the United States. However, the "Second Biggest" you can reserve to describe the London Bouillon Market Association, LBMA for short.

If you question this, check out these parameters: there is 5,000 tons of silver traded at the LBMA along with 600 tons of gold EVERY DAY. That is equal to the annual production of gold and silver in the whole world. Thus, the number of contracts sold is ONE HUNDRED TIMES the amount of actual metal sold.

Why do we call the LBMA a "Ponzi scheme?" Because it meets the first criterion of a Ponzi scheme: the promise of returns (or in this case, deliveries) that just simply can not be made.

Silver and gold supply for delivery is extremely tight and those buying bouillon must wait for weeks. We also suspect that much of the world's supply of silver in storage has been pledged to cover the paper silver. Same thing with gold.

If you question this, check out these parameters: there is 5,000 tons of silver traded at the LBMA along with 600 tons of gold EVERY DAY. That is equal to the annual production of gold and silver in the whole world. Thus, the number of contracts sold is ONE HUNDRED TIMES the amount of actual metal sold.

Why do we call the LBMA a "Ponzi scheme?" Because it meets the first criterion of a Ponzi scheme: the promise of returns (or in this case, deliveries) that just simply can not be made.

Silver and gold supply for delivery is extremely tight and those buying bouillon must wait for weeks. We also suspect that much of the world's supply of silver in storage has been pledged to cover the paper silver. Same thing with gold.

Friday, October 12, 2012

And an even wilder ride to come.

John Embry has an article (a post) in kingworldnews. KWN does not permit the reprinting of their posts, so I will summarize the situation as I see it.

There is a war between the shorts in gold (bouillon banks, the so-called commercials) and swap dealers, and others.

Currently, there are really two markets in gold: 1. the physical market in actual metal and 2. a paper market of options to buy and sell. The last reliable report pegged the paper market as ten times the size of the physical market, but I do not know if this ratio still holds.

Large and savvy traders from everywhere had large orders to fill at 1,550 and around earlier in the year, so every time the gold fixing approached that level, orders were executed to fill. Gold supply, however, gets tighter and tighter.

We saw a mini rally in gold as shorts were covering around 1,700, which brought gold prices to 1,760-1,790. It is at this level that the PM wars continue.

What propels this war? The EU needs E2T to rescue its Southern members and the FED will print $1.2T to cover the deficit and maybe another $1T to "stimulate" the economy. The FED tries to cover up its sins by "sequestering" the newly digitized money, which makes it ineffective even by Keynesian standards, which would require the money to get into the economy. Thus, the FED is simply buying time, hoping the economy will eventually recover and take credit for the recovery.

The enormous amount of money created is still there though. All that money cheapens the currencies of the participants AND THAT IS WHY GOLD PRICES HAVE RISEN. This rise has been relatively slow because of the machinations of the anti-gold faction. We are coming to a time when the manipulators will fail to control the market and then...

There is a war between the shorts in gold (bouillon banks, the so-called commercials) and swap dealers, and others.

Currently, there are really two markets in gold: 1. the physical market in actual metal and 2. a paper market of options to buy and sell. The last reliable report pegged the paper market as ten times the size of the physical market, but I do not know if this ratio still holds.

Large and savvy traders from everywhere had large orders to fill at 1,550 and around earlier in the year, so every time the gold fixing approached that level, orders were executed to fill. Gold supply, however, gets tighter and tighter.

We saw a mini rally in gold as shorts were covering around 1,700, which brought gold prices to 1,760-1,790. It is at this level that the PM wars continue.

What propels this war? The EU needs E2T to rescue its Southern members and the FED will print $1.2T to cover the deficit and maybe another $1T to "stimulate" the economy. The FED tries to cover up its sins by "sequestering" the newly digitized money, which makes it ineffective even by Keynesian standards, which would require the money to get into the economy. Thus, the FED is simply buying time, hoping the economy will eventually recover and take credit for the recovery.

The enormous amount of money created is still there though. All that money cheapens the currencies of the participants AND THAT IS WHY GOLD PRICES HAVE RISEN. This rise has been relatively slow because of the machinations of the anti-gold faction. We are coming to a time when the manipulators will fail to control the market and then...

The Case Against The Case Against Gold

October 11, 2012 In: Seeking Alpa.

By Dr Duru

Based on a quick web search, I noticed that many gold bears have written pieces with the same or similar titles. Clearly, there are common themes that embed this piece in a well-established tradition of hatred for gold. Seeking Alpha contributor Doug Eberhardt has also taken umbrage with this piece in his Instablog, and his rebuttal makes for a great read (he also posts the entire Zacks article). Eberhardt breaks things down in fine detail, point-by-point, adding lots of color. My response mainly focuses on noting how the gold bear arguments themselves demonstrate that gold is not nearly as different from other assets as the Zacks pieces suggests.

First of all, the title is a bit strange. It implies that the author thinks that markets do exist where a good case can be made for gold. In fact, the author notes that "historically, gold has been known as an effective store of value." I would have thought such a statement would end the entire debate. Instead of course there are caveats: "…but this has gone in and out of favor…The only thing that has intrinsically changed is the perception of what the future might bring." The last time I checked, bonds fall in and out of favor as well, with valuations fluctuating along with perceptions about the future. Secular and cyclical rallies, dips, and crashes are innate features of the markets we use to trade assets. Arguing that gold has a different degree of troughs and heights does not put it in a class alone. The rest of the article is full of these kinds of false differences (some repetitive). I use a problem vs. solution/comment format to highlight most of my remaining rebuttal.

Problem: "Typically, when people fear the causes of inflation, currency debasement or other potential economic downfalls, many feel it is a good time to invest in gold. Not me."

Comment: I specifically like gold as a hedge against the devaluation of the currency. The author's comments establish his position as anti-gold, but left me wondering whether this is a time when he would recommend buying gold.

Problem: "I don't see gold as a financial asset. Gold doesn't generate any income, and it doesn't pay a dividend. Thus I view it not as an investment but as a speculation."

Solution: For dividends, an investor can buy stock in a gold miner. My favorite gold miner, Goldcorp Inc. (GG), currently pays 1.2%. This may seem like trading 6 for a half dozen. However, if I look at Goldcorp's gold as simply a product that gets bought and sold according to the supplies and demands of the market, then fundamentalists can analyze it just as well as any company. Very few companies sell products that last for generations. Gold has outlasted civilizations.

Problem: "Gold's value completely depends on other people to act in a specific manner for it to go up in price."

Comment: People make markets. People must respond to bearish and bullish arguments to make any price move. Gold is no different. Stocks also depend on other people to act in a specific manner for it to go up in price. Other people must believe in the fundamentals, the technicals, and/or the theme to buy the stock. I see no difference between that and gold.

Problem: "Right now, countries around the world are trying to devalue their currency in order to improve exports and fight high unemployment. To some degree, real assets like gold should increase in price, but this idea is wholly dependent on people responding in a specific way to its inherent value, even when there's no fundamental reason to do so…The high price of gold is completely reliant on people's preferences. If those preferences change, the price of gold could fall dramatically."

Comment: This argument almost seems to contradict itself. This debasement has a potential impact on price levels throughout the economy, so it is enough of a fundamental reason to consider gold. Given gold's relatively fixed supply, its value in paper currency fundamentally increases with the amount of paper that spreads across the land. The author surprisingly admits that gold is "a real asset," but seems reluctant to accept that these debasements are a fundamental prop for price levels (including stocks!). Just like stocks, bonds, and land, people must respond in a specific way for value to get created: believe in the story of future earnings and cash flows, believe in the solvency of a company or country, believe that more and more people will find the location of your property attractive, etc. … If people's preferences for the multiples paid for earnings, for risk tolerances, or for location change, then, yes, even these assets will change in value.

Problem: "Gold is something you can hold in your hand and it looks very pretty. Buying gold is very much like buying an antique or an expensive piece of artwork."

Solution: As they say, "don't hate me because I'm beautiful." Buying gold is indeed like an antique or piece of art…except that no one uses those items as currency. The government can of course declare they have monetary value and enforce that value, but that is a flaw of any manufactured item trying to pass itself as currency, especially for pieces of paper. Gold requires no such permission. I think that gold's utility as jewelry is an added bonus to its appeal, not a detraction.

Problem: "My experience in investing has taught me that the asset class that is the hardest to own tends to perform the best. The one that's easiest, the one everyone is rushing towards, tends not to do as well."

Comment: Gold is NOT so easy to own, specifically because there are so many bears out there who are eager to see it crash. Central banks pretend to hate it even as they pile it up in reserves. The easy thing to own is paper currency. Our employers pay us with paper currency every day. With the S&P 500 at 5-year highs and bond prices at historic highs (yields at historic lows), are these assets easy to own now or hard to own? According to the logic of "anything that goes up must be too expensive," one might be tempted to dump stocks and bonds here…but of course that is not the advice given in this piece.

Problem: "The same way trees don't continually grow up into the sky, the price of gold will not continue to rise indefinitely."

Comment: This is a strange argument against gold when gold has indeed continued to rise over the long-term, generations even. I sure hope no one buys stocks and bonds because of a belief in their ability to rise indefinitely.

Problem: "Historically, when the price of gold crashes, it crashes fast."

Comment: Yes, exclude the modern day crashes in 1987, 1998, 2000, 2008, 2009, and stocks never crash fast. If gold ever crashes again, I will thank my lucky stars that I can grab it again so cheap. I sure did not buy enough back in 2008.

Problem: "In short, gold prices are being driven by 'animal spirits,' not any sort of evaluation of its intrinsic value."

Solution: If a notion of intrinsic value helps you sleep better at night, I suggest reading "Justifying Gold Prices From A Money Creation Perspective." It is a great reminder of why gold is "so high." The article also suggests, rightly so, that gold remains undervalued and under-appreciated.

Problem: "…recognize gold as something other than an investment - it is a speculation."

Response: Call it what you want, as long as gold is a store of value and a monetary unit, I am good with it.

Problem: "When everyone who has been parking their assets in gold decides it would be more productive to go into equities or other investments, the price of gold will reverse itself. Once people decide they want to stop buying the pretty rock, the price of gold will fall."

Response: This argument is a tautology. It even applies to bonds: 'When everyone who has been parking their assets in bonds decides it would more productive to go into equities or other investments, the price of bonds will reverse themselves.' Yet, even though this argument is true, no one would use it as a principle for avoiding bonds as an investment.

Problem: "What is driving the price of gold is not fundamentals, not income streams, but fluctuations and perceptions about expectations. It's essentially a speculation on mass psychology, and that, quite simply, cannot be predicted."

Response: Actually, the Federal Reserve has now made its printing rules very predictable, so I will be daring and predict gold will tend to go higher as this printing machine revs up. If the economy, GDP, stocks, and bonds were so predictable, we would all be millionaires by now.

I conclude by looking at the current setup for gold. The breakout from August 31st is well intact. While I did not interpret this year's Jackson Hole confab as a guarantee for QE3 in September, clearly a lot of people did. Gold was the first mover with stocks waiting a full week before experiencing its own breakout (to new 52-week and near 5-year highs). Just as stocks have stalled out at highs of the year, gold has stalled at its high for the year. I consider this point a rest stop for gold.

(click to enlarge)

Gold's wild ride since the last peak

Source: FreeStockCharts.com

Thursday, October 11, 2012

A snapshot of the financial world.

1. Spain.

In the news again. That's not good since the Media likes to cover only bad news. It is the next installment of the soap opera: how bad is the situation and will Spain need a bailout? Answer: the recession is deepening and yes, maybe, Spain will need some help. For comic relief, check out the story on French-Spanish co-operation agreement just signed by the Spanish PM Rajoy and French President Hollande. I guess that PM Rajoy was hankering for some good French onion soup so he traveled to Paris to sign a perfectly useless agreement.

2. Gold.

There was an attack on the gold price last Friday. It was heralded by the short interest increasing from -16,000 contracts to +14,000. The move took gold to 1,760 or so. Today, the shorts are being covered and gold is moving above 1,770 again. The supply of actual gold is tight and getting tighter. Larry has still not given a buy signal.

3. The phony jobs report.

The FED told us that it takes 240K new jobs/month to maintain employment at an even keel. The September job number was 114K, lower than the August number, which was lower than the July number. Yet, the percent unemployed magically fell to 7.8% from 8.1%. The Obama regime trumpeted this as a great success; a proof that Obamanomics is finally working. The actual figure of unemployed and part time employment remains steady at 14%. There is no improvement in unemployment.

4. The QE saga.

Nothing new to report.

In the news again. That's not good since the Media likes to cover only bad news. It is the next installment of the soap opera: how bad is the situation and will Spain need a bailout? Answer: the recession is deepening and yes, maybe, Spain will need some help. For comic relief, check out the story on French-Spanish co-operation agreement just signed by the Spanish PM Rajoy and French President Hollande. I guess that PM Rajoy was hankering for some good French onion soup so he traveled to Paris to sign a perfectly useless agreement.

2. Gold.

There was an attack on the gold price last Friday. It was heralded by the short interest increasing from -16,000 contracts to +14,000. The move took gold to 1,760 or so. Today, the shorts are being covered and gold is moving above 1,770 again. The supply of actual gold is tight and getting tighter. Larry has still not given a buy signal.

3. The phony jobs report.

The FED told us that it takes 240K new jobs/month to maintain employment at an even keel. The September job number was 114K, lower than the August number, which was lower than the July number. Yet, the percent unemployed magically fell to 7.8% from 8.1%. The Obama regime trumpeted this as a great success; a proof that Obamanomics is finally working. The actual figure of unemployed and part time employment remains steady at 14%. There is no improvement in unemployment.

4. The QE saga.

Nothing new to report.

Thursday, October 4, 2012

What happened today?

We have learned the results of two meetings today: 1. the meeting at the top of the ECB and the meeting of the FED. The FED promised to keep interfering with the bond markets longer, while the ECB reiterated its willingness to keep the Euro afloat. So, how did the markets respond?

The Euro jumped and the US Dollar Index fell over 0.5. Gold that has been struggling with 1,790, closed above 1,790 and is now near 1,800. The mining shares? They did not do so well, making Larry look a bit better.

The Euro jumped and the US Dollar Index fell over 0.5. Gold that has been struggling with 1,790, closed above 1,790 and is now near 1,800. The mining shares? They did not do so well, making Larry look a bit better.

Tuesday, October 2, 2012

And here comes QE 4.

What, you haven't heard? I am not surprised. The MSM is busy with other things.

What is QE 4? QE 4 is a continuation of Operation Twist. Though QE 4 will resemble Operation Twist, it will be different, that is not identical to it. In Operation Twist, the FED bought long term Treasuries and sold short term Treasuries on its balance sheet. That is why it could be claimed that there was no additional money added to the Money Supply. In QE 4 the FED will simply buy $45B Treasuries/month, starting Jan 1, 2013.

So, the FED will be buying $45B/mo of Mortgage-backed Securities and $45b/mo Treasuries.

One more thing. QE 4 was announced by Charles Evans of Chicago, who will be part of the FOMC Committee next year. He is credited with being the author of QE3.

What is QE 4? QE 4 is a continuation of Operation Twist. Though QE 4 will resemble Operation Twist, it will be different, that is not identical to it. In Operation Twist, the FED bought long term Treasuries and sold short term Treasuries on its balance sheet. That is why it could be claimed that there was no additional money added to the Money Supply. In QE 4 the FED will simply buy $45B Treasuries/month, starting Jan 1, 2013.

So, the FED will be buying $45B/mo of Mortgage-backed Securities and $45b/mo Treasuries.

One more thing. QE 4 was announced by Charles Evans of Chicago, who will be part of the FOMC Committee next year. He is credited with being the author of QE3.

Monday, October 1, 2012

European soap opera: Today's chapter.

BARCGHART has a news section. It "explains" why stocks go up and down. It is hilarious. It claims that today's rise of stocks in the European markets are due to the fact that Traders are buoyed by the results of the Spanish banks stress test. Really? Assuming that we can trust the results (and do we remember how the Greek reports were -ahem- fabrications?) what are these results? Why, the Spanish banks are broke and need a loan of 70+ billion Dollars. Spain itself needs over $260B, assuming that the government survives the strikes, riots and regional clamoring to secede.

The abuse of seignorage.

Seignorage is the right of those in power to make a means of exchange. In olden times this meant the minting of coins. Kings and other rulers made a small profit on doing this. Most of the coins minted were made of gold, silver or platinum and copper. But, it was inconvenient and dangerous to carry large sums of money, so paper derivatives came into use. Paper derivatives represented sums of coin, deposited at some bank.

Seignorage changed when countries began to use the derivatives as money itself. Whereas kings had to mine silver and gold to mint coins(this fact acting to restrain the abuse of seignorage), paper is very cheap, so paper money could be printed cheaply and in large quantities.

The abuse of seignorage grew with the invention of creating money digitally then creating other derivatives. Modern derivatives seldom represent value of real things, they are in fact betting slips. Stock options are derivatives of stocks, the right to own a sale or a buy of a particular stock for a stated time. Options are paper assets. There are many other derivatives: contracts to own mortgages, betting slips on interest rates, currency, bond rates. These are all paper assets. It is estimated that the sum total of derivatives exceed the value of the underlying factors by ten. Thus, the contracts to buy silver or gold is ten times the amount of the metals that are actually sold and bought.

Kings abused seignorage by reducing the metal content of coins. The modern abuse of seignorage is far more prevalent and far more dangerous. The treatment of paper assets allows the makers of tradable derivatives to add to the money supply. This in fact is an abuse of seinorage. A far more prevalent abuse of seinorage is the printing (or digitizing) of paper money to cover deficit spending. Politicians provide "free" services to constituents and pay for it by printing money. Governments following inefficient economic models cover their sins by printing more money.

The whole world is awash in paper money and derivatives. It is a colossal abuse of seignorage. It will end with the destruction of paper currencies. How soon? Hard to tell. But, the failure of paper currencies will happen almost overnight as derivatives assume their true value: the value of the paper they are printed on.

We begin to see signs of this coming. Remember the "trade" one of our banks made on derivatives? It is said to have resulted in a loss of maybe $2B. Then the loss grew to $4B and now there are hints that the loss might be as large as $100B. Allegedly, the loss has to do with trades on derivatives of interest rates. But, interest rates aren't changing much. I can think of only one area where such losses could occur: selling contracts on gold and silver. Beginning last September, gold and silver prices went down as an avalanche of sale contracts flooded the market. Did the bank deal with options to deliver? I think so. And now, with gold and silver prices having risen, the liability is rising too.

Seignorage changed when countries began to use the derivatives as money itself. Whereas kings had to mine silver and gold to mint coins(this fact acting to restrain the abuse of seignorage), paper is very cheap, so paper money could be printed cheaply and in large quantities.

The abuse of seignorage grew with the invention of creating money digitally then creating other derivatives. Modern derivatives seldom represent value of real things, they are in fact betting slips. Stock options are derivatives of stocks, the right to own a sale or a buy of a particular stock for a stated time. Options are paper assets. There are many other derivatives: contracts to own mortgages, betting slips on interest rates, currency, bond rates. These are all paper assets. It is estimated that the sum total of derivatives exceed the value of the underlying factors by ten. Thus, the contracts to buy silver or gold is ten times the amount of the metals that are actually sold and bought.

Kings abused seignorage by reducing the metal content of coins. The modern abuse of seignorage is far more prevalent and far more dangerous. The treatment of paper assets allows the makers of tradable derivatives to add to the money supply. This in fact is an abuse of seinorage. A far more prevalent abuse of seinorage is the printing (or digitizing) of paper money to cover deficit spending. Politicians provide "free" services to constituents and pay for it by printing money. Governments following inefficient economic models cover their sins by printing more money.

The whole world is awash in paper money and derivatives. It is a colossal abuse of seignorage. It will end with the destruction of paper currencies. How soon? Hard to tell. But, the failure of paper currencies will happen almost overnight as derivatives assume their true value: the value of the paper they are printed on.

We begin to see signs of this coming. Remember the "trade" one of our banks made on derivatives? It is said to have resulted in a loss of maybe $2B. Then the loss grew to $4B and now there are hints that the loss might be as large as $100B. Allegedly, the loss has to do with trades on derivatives of interest rates. But, interest rates aren't changing much. I can think of only one area where such losses could occur: selling contracts on gold and silver. Beginning last September, gold and silver prices went down as an avalanche of sale contracts flooded the market. Did the bank deal with options to deliver? I think so. And now, with gold and silver prices having risen, the liability is rising too.

Subscribe to:

Posts (Atom)