This blog will deal with large things and little things: spiritual truths, politics and economy, news, comment, food and the State of Texas. Oh, and my poetry and pictures. Enjoy.

Biblical prophecies clearly specify that the Jewish Temple will be rebuilt before the final countdown to the return of the Messiah. BUT!!! Israeli law protects the Muslim structures that now occupy what is called the Temple Mount. So, is this not a stalemate? It appears so.

However, the pressure cooker on Israel's borders are continuing to build up pressure. The terror group Hamas that controls the Gaza Strip is said to have 10,000 rockets and just suspended rocketing Israel with 500 rockets. In turn, Israel continued bombing raids against Hamas facilities. Presently, an Egyptian-brokered cease fire holds untill either side decides to break it.

On the Northern side another terror group, Hezbollah, is embedded into Lebanon and controls a wide swath of Southern Lebanon. Hezbollah has a 100,000 rockets, deployed in schools and mosques and other civilian areas. Hezbollah units have gained valuable combat experience fighting is Syria, along with Iranian and Russian troops to save Syria's Shiite government. Arraigned against them are Al Qaeda, Syrian liberationists, Saudi sponsored units and America-sponsored units.

We can really say: WHAT A MESS!

When Hamas sent rockets into Israel, the world expected a quick Israeli incursion into Hamas-held territory. It didn't happen and Avigdor Lieberman (Defense Minister of Israel and part of the ruling coalition) resigned. For a few days it appeared that this would bring on elections. That did not happen either.

What did happen is a military exercise that puts Israeli commando units in place to fight both Hamas and Hezbollah at the same time. Is this for real and foreshadows a wider war or is it simply a contrived show of force to appease the hawks in Israeli politics. Not clear till the next war. What if a couple of those rockets are off course and clear the Temple Mount?

Rep.-elect Alexandria Ocasio-Cortez (D-NY) had a few choice words for Republicans on Sunday evening, accusing them of “drooling” over her errors in “real” time. We have just two corrections to make: 1. We are not "drooling" over your uprorious and hilarious mistakes, WE ARE LAUGHING. 2. Your errors are hilarious in "real" time, slow time and any time. Salute.

Following the recent barrage of hundreds of rockets fired at Israel by Hamas, the Cabinet met and decided ...what? There was a sudden de-escalation on the Israeli side and the tanks went back to their storage places, the Minister of Defense resigned throwing the ruling coalition into a tizzy and the focus of the news went elsewhere.

What happened? We can suspect some intrigue, but what? Noi word yet, but there will be.

As time is beginning to draw a curtain over the idiotic things Nancy Pelosi says, we are discovering a new source of these gems: Alexandria Ocasio-Cortez. She comes from a district where 50% of the voters come from other countries. We are indebted to them for providing us with a source of entertainment. Alexandria, like her constituents, has no clue how this country works and indeed how most things work. That she was elected to Congress is a proof that America is a land of opportunity, even for the misinformed and the miseducated.

You think I am exaggerating? She is a Socialist and a Democrat. This is after even the Communist Party of China has abandoned Socialism. Do you compute what this means? She wants ALL of our energy needs to be met by renewables. She will start her efforts as soon as she is inaugurated (her words not mine) and will keep a sharp eye on all three branches of government: the President, the House and the Senate (again, her words not mine). There is a cartoon where she explains the difference between Capitalism and Socialism: "In Capitalism man exploits man and in Socialism it is the other way around." I am not sure if this last statement is authentic, if it is it far exceeds any words on unwisdom Nancy Pelosi ever uttered. And to show that she REALLY has no clue, she declared war on white, jurassic Democrats.

(Natural News) When the NY Times, Washington Post, CNN and other fact-challenged news outlets reported a few months ago that the oceans were warming at a catastrophic rate due to climate change, they all missed a glaring math error in the original science paper.

The paper, co-authored by Ralph Keeling of the Scripps Institution of Oceanography, was published in the science journal Nature. It erroneously claimed that ocean temperatures were skyrocketing at a rate that was 60 percent higher than the IPCC’s known rate of ocean temperature trends. But the paper suffered from a glaring mathematical error that has since been exposed.

This erroneous conclusion was immediately seized upon by the left-wing media to claim that Trump was destroying the world by promoting fossil fuels which were causing so much warming that the world would soon come to an end.

“Independent climate scientist Nicholas Lewis has uncovered a major error in a recent scientific paper that was given blanket coverage in the English-speaking media,” reports WattsUpWithThat.com, a fact-checking website that exposes the quack science behind global warming and climate change. “The paper… claimed that the oceans have been warming faster than previously thought. It was announced, in news outlets including the BBC, the New York Times, the Washington Post and Scientific American that this meant that the Earth may warm even faster than currently estimated.”

But Nicholas Lewis, an independent mathematician who fact-checks the flawed science of the climate change propagandists, found a glaring error that renders the entire conclusion of the paper — and all subsequent media reports — to be completely false.

The findings of the Resplandy et al paper were peer reviewed and published in the world’s premier scientific journal and were given wide coverage in the English-speaking media. Despite this, a quick review of the first page of the paper was sufficient to raise doubts as to the accuracy of its results.

Just a few hours of analysis and calculations, based only on published information, was sufficient to uncover apparently serious (but surely inadvertent) errors in the underlying calculations. Moreover, even if the paper’s results had been correct, they would not have justified its findings regarding an increase to 2.0°C in the lower bound of the equilibrium climate sensitivity range and a 25% reduction in the carbon budget for 2°C global warming.

Because of the wide dissemination of the paper’s results, it is extremely important that these errors are acknowledged by the authors without delay and then corrected. Of course, it is also very important that the media outlets that unquestioningly trumpeted the paper’s findings now correct the record too.

But perhaps that is too much to hope for.

“Climate change” science quacks deliberately used an incorrect data fit to mislead the public with fake science scare stories about catastrophic ocean warming

Although Nicholas Lewis publicly states that the glaring error in the original paper must have been inadvertent, most honest assessments of this junk science sorcery conclude that the “error” was deliberate deception.

Climate change scientists know full well that the dishonest media will gladly report fake science as factual and true as long as it promotes their climate change disinformation agenda. They don’t care if the facts check out. All they care about is whether President Trump can somehow be blamed (and Al Gore can be celebrated as a god, even though he knows nothing about real atmospheric science).

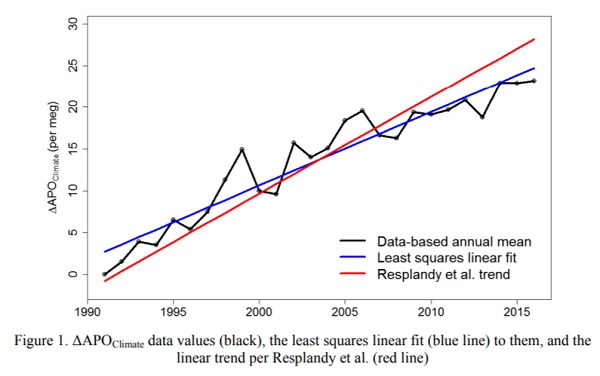

Scientific facts are of zero interest to the media, which is almost entirely run by “journalists” who are scientifically illiterate and wouldn’t know what a “least squares linear trend” is if their life depended on it.

In my analytical lab science work, we operate with multiple-point linear and non-linear fits all the time, dealing with quadratic curve fits, linear fits that exclude zero, linear fits with forced zero, fits with 1/x bias, etc. This is all basic science, yet every single journalist in the so-called “mainstream media” had zero interest in finding out whether this published science paper was actually true or not. In fact, left-wing media journalists are incapable of understand real science… or even numbers, for that matter.

As you can see in the chart below, the red line is the dishonest linear fit pushed by the quack science media. The blue line is the correct fit — using a least squares linear fit — and it shows no real change at all in the trend of ocean warming:

If you are a dishonest, scientifically illiterate left-wing journalist, you report the red line and scream about the end of human civilization caused by warming oceans. But if you’re a normal, intelligent person, you know the blue line is actually the best fit for these data.

Then again, climate alarmists aren’t interested in reporting any actual facts rooted in real science. They’re only interested in terrorizing the world population with fake science while demanding everybody pay a few trillion dollars to Al Gore and his climate skimmers, who all stand to earn insane profits by charging nations for the “right” to produce carbon dioxide.

Meanwhile, intellectually dishonest liberals flat-out refuse to examine real scientific facts on climate

Further demonstrating their own intellectual dishonesty, liberals absolutely refuse to examine any real facts on so-called “climate change.”

To any unprejudiced person reading [Goklany’s] account, the facts should be obvious: that the non-climatic effects of carbon dioxide as a sustainer of wildlife and crop plants are enormously beneficial, that the possibly harmful climatic effects of carbon dioxide have been greatly exaggerated, and that the benefits clearly outweigh the possible damage.

I consider myself an unprejudiced person and to me these facts are obvious. But the same facts are not obvious to the majority of scientists and politicians who consider carbon dioxide to be evil and dangerous. The people who are supposed to be experts and who claim to understand the science are precisely the people who are blind to the evidence. Those of my scientific colleagues who believe the prevailing dogma about carbon dioxide will not find Goklany’s evidence convincing. I hope that a few of them will make the effort to examine the evidence in detail and see how it contradicts the prevailing dogma, but I know that the majority will remain blind. That is to me the central mystery of climate science. It is not a scientific mystery but a human mystery. How does it happen that a whole generation of scientific experts is blind to obvious facts? In this foreword I offer a tentative solution of the mystery.

The climate change delusion, in other words, is a kind of irrational denialism by the scientific establishment which has destroyed its own reputation by refusing to embrace real facts. Instead, the quack scientists of climate change are pushing a political agendaand dressing it up to look like science, when in reality it isn’t science at all.

Dyson goes on to explain:

There are many examples in the history of science of irrational beliefs promoted by famous thinkers and adopted by loyal disciples. Sometimes, as in the use of bleeding as a treatment for various diseases, irrational belief did harm to a large number of human victims. George Washington was one of the victims. Other irrational beliefs, such as the phlogiston theory of burning or the Aristotelian cosmology of circular celestial motions, only did harm by delaying the careful examination of nature. In all these cases, we see a community of people happily united in a false belief that brought leaders and followers together. Anyone who questioned the prevailing belief would upset the peace of the community.

Indur Goklany has assembled a massive collection of evidence to demonstrate two facts. First, the non-climatic effects of carbon dioxide are dominant over the climatic effects and are overwhelmingly beneficial. Second, the climatic effects observed in the real world are much less damaging than the effects predicted by the climate models, and have also been frequently beneficial. I am hoping that the scientists and politicians who have been blindly demonizing carbon dioxide for 37 years will one day open their eyes and look at the evidence.

Dyson is going to be waiting a very long time, of course, for scientists to open their eyes and look at the evidence. That’s because climate change has never been about the evidence. It remains solely about the political power to be found in condemning carbon dioxide as an atmospheric poison when it’s actually planet Earth’s most important life-giving nutrient for plants, forests and food crops.

The climate change cultists, in other words, are not scientists. They are propagandists posing as scientists, but since their conclusions support the quack science dogma of the globalists who seek to enslave humanity under a scientific dictatorship, they go along with it.

If you want to read the full report by Indur Goklany that’s being described here by Freeman Dyson, you can find it at this link (PDF) from the Global Warming Policy Foundation.

When scientists like Dyson find the courage to speak out against the climate change nonsense, it’s a sign that things are beginning to turn. It’s no longer just the Health Ranger and other independent scientists who are exposing the lunacy of the climate change narrative; it’s now some of the most celebrated personalities in the institutions of modern science.

The Fed increased its scheduled bloodletting of the banking system to (up to) $50 billion per month in October. We’ve seen the effects.

The Fed calls this program “normalization” but I call it “bloodletting,” in honor of the medieval medical treatment for disease. That barbaric treatment used leeches to suck the blood from sick patients. The Fed is bloodletting bloated financial asset bubbles by shrinking its balance sheet. It is letting assets mature and is redeeming them, which gradually reduces the size of its balance sheet to normal levels.

Most importantly, as it redeems its holdings, that sucks money out of the banking system.

Click here to see how this works, why it’s so important to the health of your capital, and what you can do to profit from it.

The Fed’s Two Pronged Attack Is Sucking The Market’s Blood

To achieve its ends, the Fed is doing two things.

First, it has now essentially ended its purchases of MBS (mortgage backed securities) from Primary Dealers. It had been buying MBS to replace the MBS that were prepaid (paid down) each month. That goes on in the normal course of business as borrowers pay off existing loans. Without the replacement purchases, the Fed’s MBS holdings will shrink. The amounts will vary according to the total mortgages paid off by borrowers each month, whether through new purchase mortgages, refinancing, or other payments.

Again, here’s what’s important. As borrowers pay off the mortgages held within the MBS, that extinguishes a like amount of deposits in the banking system.

Secondly, as of October the Fed is allowing up to $30 billion per month of its holdings of Treasury notes and bonds to mature. Prior to the start of the bloodletting in October 2017, the Fed had always rolled over all of its Treasury holdings. It thus extended the loans it had made to the US Treasury. No more! The Fed is now telling the US Treasury, “Pay us back $30 billion per month!”

Money Disappears from the System When The Fed Shrinks Its Balance Sheet!

To get the cash to pay off the Fed, the Treasury must borrow that money in the market. It must sell debt to investors and dealers. As they purchase the new debt from the Treasury, they withdraw the cash from their bank accounts and pay the US Treasury in exchange for the new debt paper, whether Treasury bonds, notes or bills.

The Treasury simultaneously pays off the Fed for the notes and bonds the Fed is redeeming. The assets on the Fed’s balance sheet shrink and, more importantly, the money leaves the banking system for good when it is used to pay off the Fed.

That’s how the Fed’s balance sheet “normalization” causes the amount of money in the system to fall and financial market conditions to tighten. It has been most evident in soaring T-bill rates over the past year. But lately, it has been showing up in stock prices too.

As the Fed drains money from the system, there is less and less of it available to absorb the constant flood of future Treasury supply. Dealers and investors are forced to liquidate other assets to absorb the crush of the new supply. Those liquidations cause the prices of all financial assets to fall. Bonds have been in a bear market since 2016. The bear market in stocks is only beginning.

The actual amounts paid down depend on Treasury maturity schedules and mortgage market conditions. As mortgage rates rise, mortgage payoffs slow down, which slows the Fed’s balance sheet reductions.

How The Fed’s Shrinking Balance Sheet Pressures the Markets

But that doesn’t matter. Whether the amounts redeemed are $30 billion or $50 billion per month, the effect of the drains in the market are cumulative. Any amount of Fed drains is now just another turning of the screw squeezing the markets.

As JP Morgan famously said, “The Fed’s balance sheet will fluctuate!”

Actually he said, “The market will fluctuate.” But hey, let’s not quibble. From 2009 to 2017, the Fed was the market. It pumped $3.7 trillion in new, zero cost, money that it conjured up out of the ether, into the accounts of Primary Dealers. It rightly expected the dealers to use that cash to buy stocks and bonds, bidding up their prices and setting off a speculative frenzy that lasted nearly a decade. Since 2017 however, the Fed has not only stepped back from inflating the market, its draining operations are indirectly causing the market to deflate.

In early October I wrote in the Wall Street Examiner, “A growing shortage of money will eventually result in a bear market in stocks that won’t end until the Fed reverses policy. “The exact pace of these drains does not matter. This is not a case of the Fed pulling cash directly from dealer accounts. QE was added directly to the market via trades with Primary dealers with cash flowing into their accounts. That was a measurable, predictable, direct impact. Under the Fed’s balance sheet bloodletting, the effect on the stock market is indirect, diffuse, and delayed. ” Very delayed. Investors have decided that they will use whatever remaining cash they have to buy stocks. And they’ve decided to use leverage on top of that… When this burns out, the turn will be violent and merciless because the cash to support the markets will simply no longer be there.

The teacher asks the students about what their Father does for a living. When it comes little Johnny's turn he is reluctant. After encouragement from the teacher Johnny blurts out:"He is a stripper in a gay club and does tricks in the alley afterward." After the class is over the teacher asks Johnny "is your Father really a stripper?" "No," answers Johnny, "he is a Reporter for CNN, but I was too embarrassed to say that."

AJ begins: California has passed into a land where the vestiges of America's founding ideas are barely alive. 'Progressive' policies are beginning to devastate the countryside. What isn't destroyed by the 'Progs' is threatened by by natural forces: fires, followed by deluges and mud slides and eventually earthquakes. Such is the fate of a land that turns its back on God. He withdraws His protection from them.

One of these plaques is typhus. It is brought on by...well, read this article from the D.C. Clothesline Alert.

California’s Typhus Surge Is Linked to Fleas, Feces, and Bad Economic Policies

Typhus is on the rise in Los Angeles, with its epicenter in downtown, where the city’s sanitation officials are struggling to respond to the nearly two thousand “cleanup requests” they get from locals every month.

Like San Francisco, LA is struggling to clean up city streets of human waste—specifically feces—due to a lack of public restrooms and a growing homeless population.

There was an average of 700 requests in the area in the spring of 2016, but officials now claim they receive about 1,900 cleanup calls per month thanks to the number of growing homeless camps. But the growing homelessness and sanitation nightmares have led to yet another crisis: a rise in flea-borne typhus.

Typhus Outbreak

Between July and September, county officials identified at least nine typhus cases that originated in downtown. At least six of the infected were homeless, but central LA isn’t the only place at risk.

Officials in the city of Pasadena, also located in Los Angeles County, claim 20 residents had typhus fever this year. Typhus cases have also been registered in Long Beach and Willowbrook.

As the number of cases continues to rise, the Los Angeles County Board of Supervisors feels pressured to act. They recently voted on a pilot program to fight the illness in homeless encampments by adding more cleanup efforts, introducing more mobile showers, offering the homeless housing, and distributing hand sanitizer and flea repellent for people and pets.

The crisis, which has already made 64 victims this year alone, has deeper roots. At least, that’s what 5th District Supervisor Kathryn Barger appears to claim.

“When I drive through parts of my district and I see the living conditions on the street, it reminds me of a third-world country,” Barger said.

Perhaps the fact that California falls behind every single state in the country when it comes to fiscal, regulatory, tax, and economic policies—much like many “third-world” countries—has something to do with the current conditions residents are now forced to grapple with.

California Isn’t Serious about Ending Homelessness

As the Cato Institute’s Freedom Index reveals, California’s suffocating regulatory environment has a series of very real and heartbreaking consequences.

When it comes to land-use freedom, for instance, cities like Los Angeles have restrictive rules regarding housing supply and rent control, keeping builders from developing affordable housing and helping to artificially increase the cost of housing across the board.

But bad housing policies are not the only cause of growing homelessness in Los Angeles. The state’s labor laws add insult to injury by making it difficult for employers to help those in need. With high minimum wage laws, no right-to-work policies in place, mandated short-term disability insurance, and prohibiting consensual noncompete agreements, job creation in California is dramatically held back, and the poor and low-skilled are unable to break into the labor market.

In addition, occupational licensing also keeps entrepreneurs from entering the market due to the extensive cost associated with obtaining the mandated training and certification to perform simple services.

With state lawmakers being so eager to get involved in every single affair, from banning straws to keeping residents on a budget from using scooters, it’s hard to see how these rules could be repealed—or at least reformed—anytime soon.

As the founder and president of the Future of Freedom Foundation Jacob G. Hornberger explained, the root causes of homelessness in most major urban centers across the US are both minimum wage laws and zoning, two policies that are not only in effect in California but that have been revamped and strengthened again and again over the years.

With California residents once again helping progressives stay in power in the region, we know these policies are not going anywhere. If anything, they will continue to receive widespread support from the newly-elected governor.

For the time being, there might not be a government-backed solution to Los Angeles’ typhus outbreak, but if the city’s and state’s politicians really want to end homelessness, then repealing zoning and minimum wage laws would be a great start.